The policies of the Trump administration following Brexit and possible political change in Europe in the near future could lead to unprecedented change in Ireland. Despite the narrow immediate focus on the possible effect on U.S.foreign direct investment, longer run implications for world economic stability, for society, and political governance are likely to be far more important.

Proposed changes that have attracted considerable media attention (for example in this piece by Cliff Taylor in The Irish Times) are a reduction in the U.S. corporate tax rate from 35% to 15%.

Unrepatriated earnings held in cash would be taxed at 10% and other earnings at 4%.

These proposals are similar to those made by the Obama administration, who proposed a tax on unremitted profits of U.S. companies of 14%, a continuing tax of 19% and a reduction in the standard rate of corporation tax to 28%. This proposal also envisaged that 85% of tax already paid could be credited against U.S. tax due.

The effect on corporate tax strategies

The proposed Trump changes, if introduced, could have a dramatic effect on U.S. Multi-National Enterprises (MNEs) corporate tax strategies. The effects on real investment are more difficult to understand.

Incentives for inversions are reduced but not entirely eliminated as nominal tax rates in some countries will remain below those proposed U.S. profits and on unrepatriated profits of U.S. companies.

U.S. tax changes could result in some increase in nominal corporate tax rates in low tax countries as there is an incentive to raise corporate tax rates (and tax revenue) if most of the tax paid could be offset against U.S. taxes due. As tax regimes that enable low or zero tax rates are reduced within the EU (for example stateless income and double Irish tax strategies will be made more difficult) there could also be an incentive for U.S. firms to reallocate investment.

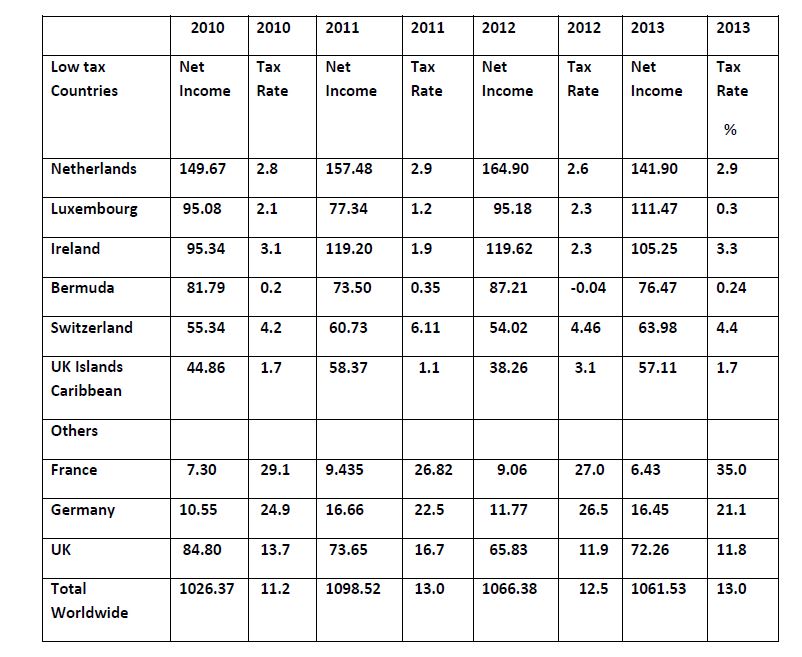

These effects will depend on the effective tax rates rather than nominal tax rates in both the U.S. and countries where FDI locates. U.S Bureau of Economics Analysis' data is the most comprehensive data base on U.S. MNE’s as shown in the table below (click on the table to enlarge).

The table shows that the Netherlands is consistently the country where the largest U.S. MNE income is declared over the period 2010-2013. This is followed by Luxembourg and Ireland for 2013. Effective tax rates have varied between 1.9% and 3.1 % for Ireland and are slightly lower for the Netherlands.

(1) Defined as tax paid/(net income plus tax paid).

(2) The fall in income for Ireland between 2012 and 2013 is explained by the inversion of U.S. based companies to Ireland

Source: Bureau of Economic Analysis Table II.D 1, Income Statement for majority owned affiliates 2010-2013.

There is a large difference in effective tax rates comparing the main EU countries with tax haven type features (Ireland, Luxembourg and the Netherlands) and no-tax jurisdictions such as Bermuda.

Finally the table shows that France (35%) and Germany (21.1%) followed by the UK (11.8%) have much higher effective tax rates. Even though effective tax rates are higher in France, because far greater income is declared in Ireland, tax payments in Ireland ($3.58 billion) for 2013, are higher than In France ($3.45 billion).

US firms in Ireland likely to pay little extra tax

As tax rates in Ireland are similar to the Trump proposed U.S. tax on foreign earnings of 4%, U.S. firms in Ireland will pay little extra tax, assuming the Irish tax paid can be offset against any U.S. taxes due.

One interesting implication for U.S. companies operating in high tax countries such as France, is that tax credits may be used to offset taxes due in the U.S. This possibility may result in limits on the extent to which foreign tax credits may be offset against U.S. taxes.

A second blog tomorrow will discuss possible implications for real investment.

Prof Jim Stewart

Dr Jim Stewart is Adjunct Associate Professor at Trinity College Dublin. His research interests include Corporate Finance and Taxation, Pension Funds and financial products, Financial Systems and Economic Development.

He is widely published and his titles include Mutuals and Alternative Banking: A Solution to the Financial and Economic Crisis in Ireland (2013), Choosing Your Future: How to Reform Ireland's Pension System (co-author, 2007) and For Richer, For Poorer: An Investigation of the Irish pension system (2005).

Share:

![Duggan, Vic]](/assets/img/2017/04/1491994913319631_sq.jpg)