Paul Sweeney: Here on Progressive Economy, we have been examining the evidence for tax reform in recent months. In my last Blog I looked at employees’ social insurance and here I examine employers’ social insurnace.

Is Ireland “the best little country in which to do business”? It has the lowest corporation taxes in the EU, no corporation taxes for some multinationals who chose to use aggressive tax planning and very low social charges on employers. And we had very low average income tax rates though they were increased – but only to the OECD average since the Crash of 2008.

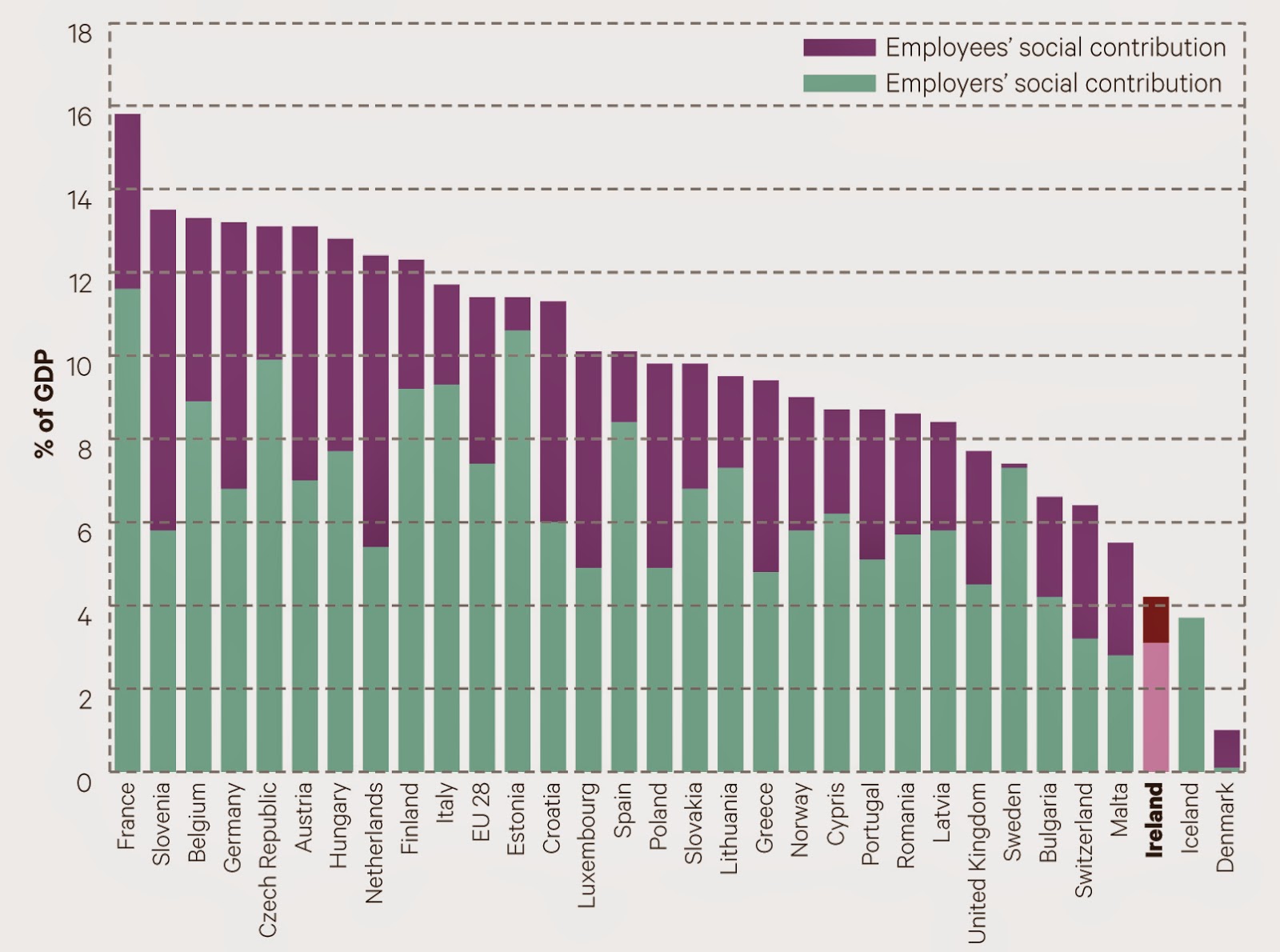

The Table below from the OECD data published in March 2015, shows how low employers’ social charges are in Ireland in 2014 and for other years and countries selected. I took 2002 as it was the year in which the employers’ rate was reduced in Ireland to its current rate.

It was in 2002, during a jobs boom, the already low employers social charges were reduced to 10.75% of the earnings – a classic pro-cyclical act by Mr McCreevy. Our rate is 7% below the OECD average but much lower than in most of the original EU15 states with which most comparisons are made. It is highest is France at over 38% and Sweden is high too at 31% but a few are in the high 20s.

Since the Crash, the rate of VAT has been increased and income tax and employees’ (only) social charges like the USC have also been increased.

Corporation tax rate, which used to be 50%, was progressively reduced to a nominal maximum rate of 12.5% in 2002. It has not been increased since then in spite of the Crash. This a key part of Ireland’s low tax strategy to attract FDI. Yet, the revelations that this is the maximum rate and that a great number of highly profitable companies pay nowhere near this modest level, has not lead to any new policy consideration on this matter.

In fact, with new subsidies for R&D and “Patent Boxes”, the effective rate of Corporation Tax has actually been reduced since 2002, while taxes on citizens have been increased.

The simplistic argument in favour of low social charges is that they are a disincentive to work and “destroy jobs” was dissected by Oisin Gilmore in a recent Blog. This very strong word “destroy” is used by the Right in this context. Yet the rates are higher in most Nordic countries (excluding Denmark – not on table - where they are zero – being paid out of income tax). And they have higher employment rates than we have and lower unemployment. The argument also ignores equity and other principles of taxation. It is simplistic but suits a purpose for some.

Also why increase charges paid by employees and income taxes but not get employers to contribute anything to redressing the crisis? Both have been pro-cyclical, but deemed necessary – for employees only.

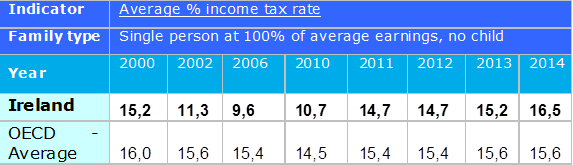

This table shows the average rate of income tax paid by a single person with average earnings average in Ireland and a comparison with the average of the OECD.

It can be seen how low average income tax rates were reduced to during the bubble in Ireland to an extraordinarily low level of only 9.6% in 2006 at the height of the Boom. In fact, just before the Crash of 2008, the rates were down to 8.7% for 2006 and 2007 (not shown).

In contrast, the average tax rate hovers around 15 or 16% in OECD [which includes some low income average tax rate countries like Korea (5% in 2014), Japan (7%), Israel (8.6%), Slovak (9.4%) and Greece (8.9%) as well as some high rate countries, Denmark (35.6%) and Belgium (28.3%).]

In conclusion, this is a great little country in which to do business.

But with such low taxes on business in contrast to other states, why is unemployment so persistently high, if low taxes on companies equals jobs, as some assert? The employer social contribution rate is - in my opinion - too high in some states and too low in others, including Ireland.

Secondly, it was seen that average income taxes paid by workers were reduced by Mr McCreevy during the bubble to very low rates and they have been raised since the crisis, but only to OECD average rates - which are still well below those rates in most of the more developed EU countries.

Paul Sweeney is Chair of TASC's Economist Network

Paul Sweeney @paulsweeneyman

Paul Sweeney is former Chief Economist of the Irish Congress of Trade Unions. He was a President of the Statistical and Social Enquiry Society of Ireland, former member of the Economic Committee of the ETUC, a member of the National Competitiveness Council of Ireland, the National Statistics Board, the ESB, TUAC, (advisor to OECD) and several other bodies. He has written three books on the Irish economy and two on public enterprise, including The Celtic Tiger; Ireland’s Economic Miracle Explained and Selling Out: Privatisation in Ireland, chapters in other books and many articles on economics.

Share:

![Duggan, Vic]](/assets/img/2017/04/1491994913319631_sq.jpg)