Michael Burke: In the furore about the recent Morgan Kelly article in the Irish Times, in which he advocates a debt default, there has been very little light and much heat generated. The worst response I have seen (there may be others), in terms of lack of logic, was that from former Taoiseach John Bruton, who argued that the ECB would go bust if this state defaulted on any part of its debt. Some should tell the chair of the IFSC Ireland that central banks can’t go bust from a default in the currency which they produce.

But there was one chink of light. Strangely, the NTMA has issued an ‘Information Note on Ireland’s Debt’. No-one can recall one these strangely-titled notes ever having been issued before. For any information on this topic we should be grateful, although it seems some of the thanks should be directed towards Prof. Kelly.

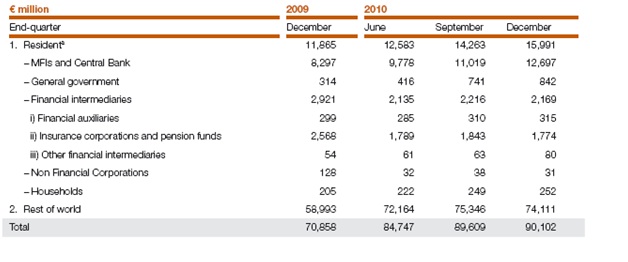

In the note, point 3, it refers to the holdings of government debt by residency, and produces a truncated version of a table that first appeared in the Central Bank’s Quarterly Bulletin. Below the fuller version from the Bank’s Bulletin is reproduced (Table E3).

The table shows this concern to be misplaced. TotaI government debt at the end of 2010 was €90.1bn. If we take only Irish residents, the overwhelming bulk of the €16bn in debt held was by MFIs (monetary financial institution; banks) and the central bank. Only €252mn was held directly by households and a further €1.774bn mainly on their behalf by insurance and pension funds. So, just over €2bn held by Irish ‘widows and orphans’- most of whom aren’t, of course. Many will be very wealthy individuals who have built substantial private pensions to supplement their not-ungenerous state pensions, mainly via a tax cost to the Exchequer, ie other taxpayers.

The holdings of pensions and insurance funds have fallen significantly over the last year from already low levels. This reflects the exit of mainstream investors from the Irish government bond market. We were repeatedly told that cuts to government spending would restore the confidence of the markets. The measures of confidence are that Irish 10yr yields are now at a new high of 10.65% and the ratings’ agencies have downgraded sovereign debt again, to one notch above ‘junk’ status.

Most mainstream investment funds, certainly any managing pensions, are prevented by their investment restrictions from investing in such low-grade debt. The high yield on the debt reflects the exit of these investors. The recent downgrades are likely to produce a further decline in these holdings. But, since every sale requires a buyer some other type of entities must be increasing their holdings. Among residents this increase has been by MFIs and the central bank.

The bulk of government debt is held overseas, €74bn of €90bn. While the ECB has increased its holdings of government debt, this has been almost exclusively in the form of collateral posted by Irish and other banks in return for short-term lending from the ECB. The same investment restrictions on junk or near-junk apply to European mainstream funds as to Irish ones. They too will have been forced to divest as the credit downgrades were accumulating.

Therefore, the new buyers cannot have come from the ranks of mainstream investors. The types of funds that can purchase near-junk debt are specialist funds in ‘distressed debt’ sometimes known as vulture funds, hedge funds and others. These are not the savings vehicles for widows or orphans, but for the extremely rich.

Turning to bank debt, the same argument applies with even more force. All the main deposit-taking Irish banks have been downgraded to junk status. Mainstream investors are simply not allowed to invest in their debt- their investment mandates preclude it. The holders of that debt, aside from central banks and each other, will therefore be the same roll-call of parasitic speculators.

It is also to these funds that Irish taxpayer will be paying the proceeds of ‘promissory notes’ to fund Anglo Irish debts. This will incur €3.1bn per annum for a total cost of €43.3bn until 2015, assuming a very favourable fall in government borrowing rates. Anglo is not now and never has been a bank which performed any useful function and there is no logical reason for taxpayers to accept this imposition.

A chink of light has been let in on the State’s debts. What is revealed reinforces the case for default.

Share: