Tom McDonnell: The new Programme for Government is, perhaps understandably, light on detail in many areas. The document is highly aspirational in nature and it remains to be seen whether the numbers stack up in the short or medium term. Making the numbers ‘fit’ will undoubtedly determine the fate of the numerous policy goals stated in the Programme and will also condition the decision-making process around the existing policies up for review in the next few months.

One policy decision which captured much public interest in the last few months was the decision to replace the health levy and the income levy with the new Universal Social Charge.

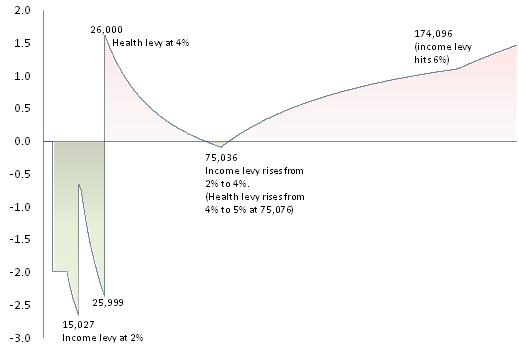

The combined impact on gross earned income from the introduction of the new Universal Social Charge and the abolition of the Health Levy and the Income Levy are shown in Figure 1. The earner worst affected by the changes in terms of percent of gross income is the individual on €15,027 (the old income levy kicked in at €15,028). He or she will lose 2.66% of income from the combined changes.

On the other hand the biggest winners from the combined changes (other than those on very high incomes such as Government Ministers and Secretary Generals) are those on just over €26,000. This is because the old health levy kicked in at 4% on the entire amount at €26,000.

Figure 1

Combined impact as percentage of gross income (single employee aged 16-65) - winners in pink and losers in green (click to enlarge)

The overall regressive nature of the changes shown in Figure 1 is stark. Page 2 of the Programme for Government makes the laudable statement that

“Both our parties are committed to protecting the vulnerable and to burden sharing on an equitable basis”.

In page 16 of the same document the Government commits to reviewing the USC. Page 16 also promises to maintain the current rates of income tax together with bands and credits. Consequently, and in the context of the severe budgetary constraints, we can assume that any changes to the USC will either be implemented on a revenue neutral basis or (more likely) implemented in a way that increases net revenue.

Let us hope the new Government’s commitment to “protect the vulnerable and ensure burden sharing on an equitable basis” guides their thinking when they make their changes.

We watch with interest.

Dr Tom McDonnell

Tom McDonnell is senior economist at the NERI and is responsible for among other things, NERI's analysis of the Republic of Ireland economy including risks, trends and forecasts. He specialises in economic growth theory, the economics of innovation, the Irish and European economies, and fiscal policy. He previously worked as an economist at TASC and before that was a lecturer in economics at NUI Galway and at DCU. He has also taught at Maynooth University.

Tom obtained his PhD in economics from NUI Galway.

Share: