Michael Taft: One might expect a pre-budget submission in today’s climate to focus on how to ‘save’ money through a lengthy list of public spending cuts combined with tax increases that ‘broaden the tax base’ (that used to refer to high income groups who escaped liability through exploiting tax avoidance mechanisms; not anymore: low-income groups are now the main culprits). Such a submission would then tally up column A and column B and see if the difference brings down that danged deficit. And in the coda, the submission would don ceremonial robes and prostrate itself before the financial markets for fiscal blessing.

Thankfully, TASC produced its own pre-budget submission.

The temptation is to start listing off particular elements one likes or doesn’t like but that approach is not satisfactory. Progressive groups and individuals can produce pre-budget submissions until the end of the time which, while adhering to the same principles, will never agree on the details. As President Franklin Roosevelt said, ‘There are many ways to go forward, there’s only one way to stand still.’

It is far more helpful to stand back and look at the overall composition, the architecture. TASC’s submission rests on two broad pillars:

1. Drive budgetary consolidation through taxation – primarily, reduction of tax expenditures and a residential property tax. The total amount to be raised is €2.7 billion. The underlying principle is to break from the low-tax model and move, over time, to average EU taxation levels.

2. Drive economic growth, employment and, so, deficit reduction through a €3 billion Economic Recovery Fund to be financed from the National Pension Reserve Fund (NPRF).

This is complemented by a number of proposals to increase budget transparency and improve budget documentation. There are some well-considered public efficiencies (e.g. reduce subsidies to fee-paying schools, etc) amounting to €300 million.

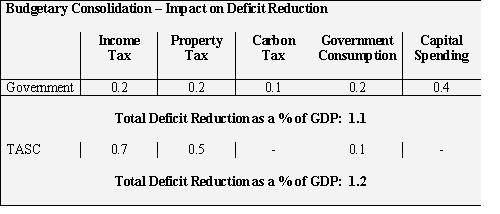

So what would the effect of this be in terms of the economy and public finances? Let’s measure it using the ESRI multipliers and compare it with the Government’s original €3 billion package (the ESRI set up a stylised budget for measurement purposes as details of the package’s composition were, naturally, not available).

Just on the budgetary consolidation measures alone, the TASC package is superior. Indeed, it would work out better in practice. First, TASC is rightly aiming at high income groups which would prove less deflationary than ESRI estimates as these assume across board tax increases. This would therefore increase the deficit reduction. Secondly, ESRI warns that its numbers ‘do not take account of the significant positive supply side effects from public investment’. This suggests significant losses to the Exchequer in the medium-term, diluting the deficit-reduction in that category.

However, TASC goes further, transcending the narrow balance sheet mind-set; it actually acknowledges such a thing as the economy – the economy that is the basis for any credible fiscal consolidation process. Their Economic Recovery Fund of €3 billion would start to address our considerable deficits: credit availability, infrastructural capacity, R&D, human resources, etc.

Measuring these impacts is a little more difficult. Traditional multipliers measure investment, non-wage consumption, social transfers, tax cuts, etc. The TASC programme contains programmes such as loan guarantees – which would have a definite economic benefit. However, it is not easy to measure under headline multipliers. In order to draw a conservative baseline, I will include only the infrastructural and education component – acknowledging the remainder as part of a general upside risk, always a good thing to have when entering an uncertain period. When these are included we find:

This is a significant turnaround. Instead of the Government’s deflationary budget with significant downside risks, we have an expansionary one with significant upside risks. And with no extra borrowing. As a result the deficit reduction is much higher than what the Government is proposing.

There’s another significant advantage that TASC delivers: it might be called Deflationary Cascade Avoidance (DCA). By providing an alternative to the current deflationary approach, we may be avoiding what the Government is leading us into – and highlighted by Michael Burke in his analysis of the submission. Michael refers to the IMF finding that fiscal contraction in situations where there is no scope for reducing interest rates further, will suffer a double whammy. A 1 percent fiscal contraction could actually double the deflationary impact – from -1.1 to -2 percent.

Were this to occur, we may be entering into a long-term deflationary trough where growth is sluggish at best and there is no chance of halting the rise in debt and interest payments; stuck in the proverbial creek without a paddle or a boat on a moonless night with the sound of large predators on shore. TASC’s DCA ensures we can be at home, sleeping in our beds.

No doubt the cheerleaders for fiscal contraction will ignore all this. They will ignore the benefits of the TASC submission; they will ignore the ESRI finding that the current strategy will fail to repair public finances for a decade and more and drive up debt to 1980s level and beyond; they will ignore warnings from international bodies about the course we are heading on. If they get their way, we will all sleepwalk into IMF receivership and years of deflationary slump.

We can’t let this happen. We have to start fighting back sometime. Now is not too late.

And we have increased our chances of winning now that TASC has given us this new weapon in the form of the pre-budget submission.

Michael Taft @notesonthefront

Michael Taft is an economic analyst and trade unionist. He is author of the Notes of the Front blog and a member of the TASC Economists’ Network.

Share: