Michael Burke: One of the strange features of the debate on the economy and government finances is that the consensus has solidified around further deep cuts in public spending even as the evidence mounts that this policy is wholly counter-productive. We are told repeatedly that it is impossible to invest our way to recovery because it would lead to a wider deficit, higher bond yields and even being shut out of the international markets altogether. Yet all this has come to pass while a fiscal contraction equivalent to 9.1% of GDP has been implemented. A further €4.5bn in cuts this year would bring this total fiscal contraction to approximately 12% of GDP.

Therefore the contribution from TASC to the 2011 Budget debate, Investing in Recovery, Jobs, Equality, is extremely welcome. Breaking entirely from the dominant misconceptions that spending cuts will restore either the economy or government finances, the proposals centre on tax increases for the wealthy and spending increases to boost jobs.

Tax increases for the wealthy are not simply about fairness, although it is monstrously unfair for PSRI contributions to be capped on salaries above €75,000 and not to be levied at all on unearnt income on financial and other assets. Personal consumption has fallen by nearly 11% and €10bn in real terms in the course of the recession. These income groups have the lowest propensity to consume of all, and the redistributive effect of higher, fairer taxes on the rich while boosting employment will be to increase overall demand in the economy.

Increased spending to maintain and create jobs would have a decisive effect on both economic activity and the Budget deficit. TASC proposes a €3bn Economic Recovery Fund, financed by funds from the NPRF. This would be an important contribution to addressing the real decline in investment during the recession, a fall of €22bn, down 49%.

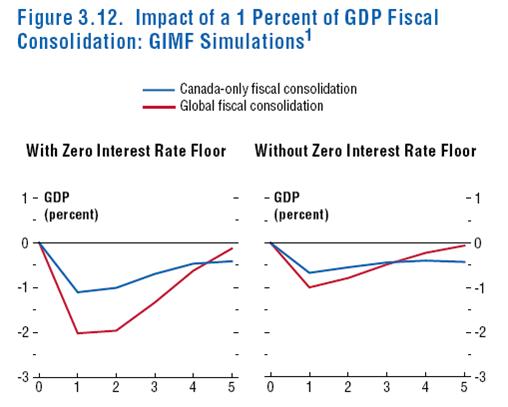

'What would be the effect of such a policy? Thanks to Philip Lane on Irish Economy, who provides a link to an IMF paper, Will It Hurt? The Macroeconomic Effects of Fiscal Consolidation. Its author Daniel Leigh spoke at a TCD on October 14th. The Irish Times carries this report, which includes this important point, “The research also points to the negative effects of fiscal tightening being twice as large in the absence of monetary loosening (ie cuts in interest rates). It is twice as large again if fiscal tightening is taking place simultaneously elsewhere".

The charts below highlight those propositions, that the negative impact of public spending cuts is doubled when there is no ability to cuts interest rates simultaneously, and increased too by simultaneous fiscal tightening globally, as is currently the case. (Canada is chosen because of its openness).

Crucially, those two conditions apply to this economy currently, an inability to lower interest rates (in fact Irish market rates are rising) and the negative impact of simultaneous public spending cuts elsewhere. It can be seen from the charts that the response to a fiscal tightening equivalent to 1% of GDP lowers GDP by 2% in the first year alone. Cumulatively, the IMF research shows that over 5 years the lost output is approximately 6% of GDP.

Any shock which lowers output by 6% will of course negatively impact government finances, by far greater than the initial 1% ‘saving’. This is precisely what has happened- spending cuts have led to a wider deficit.

These responses tend to be symmetrical; the change induced is the same positively or negatively. So, to take TASC’s €3bn in investment, this IMF estimate suggests it would have a €6bn positive impact in the following year and provide a cumulative boost of approximately €18bn.

What then of government finances? This would need to be based on both parts of the public sector accounts, increased tax revenues from higher levels of activity and lower welfare payments as people are brought back into work and poverty declines. The DoF estimates that the sensitivity of public finances to changes in output is 0.6. So, government finances would improve by €3.6bn in the following year (€6bn X 0.6) and by €10.8bn cumulatively (€18bn X 0.6).

That’s a genuine deficit-reduction plan based on growth.

Share: