Michael Taft: ‘The bank is something more than men, I tell you. They breathe profits; they eat the interest on money. It's the monster. Men made it, but they can't control it.’

So wrote John Steinbeck in The Grapes of Wrath. It could easily be applied here (except for the profits part – but the Government is doing everything possible to get them back into the black with our money).

So how do we slay, or at least cripple, the biggest monster of them all – Anglo Irish? Jim Stewart has put forward an incredibly simple, practical and far-reaching proposal that can save the taxpayers’ billions (this was followed up by Brian Lucey).

In its Recovery Scenario the ESRI estimated that the bail-out of Anglo-Irish and Irish Nationwide would cost a combined €25 billion. We have moved on a bit, but let’s take the ESRI’s calculations as a proxy for Anglo alone (it will serve the purposes of this analysis). It will cost, when the bail-out is fully paid over, approximately €1.25 billion a year in interest payments.

But there is an additional, even more substantial, drain. The ESRI estimates that the banking crisis could contribute up to 15 to 20 percent of the permanent loss of output due to the recession. We won’t factor this in (partially because it will only be permanent if we persist with current policies) but the ESRI warns us that this indirect cost could be substantially higher than the direct costs in terms of lost revenue and higher unemployment costs.

Now, let’s take up what I call ‘Jim’s Equation’. Simply put, Jim argues that we should:

‘ . . negotiate with all bond holders and purchase bonds, not at face value but at some fraction of face value. Writing down the 2009 balance sheet value of Anglo Irish debt by 50% would reduce balance sheet liabilities by €8.7 billion. Writing debt down to 10% of face value (a generous value in the event of liquidation) would reduce balance sheet liabilities by €15.6 billion.’

Jim, along with Professor Louis Brennan, makes the same point in the Financial Times:

‘A more effective approach from the perspective of Ireland’s taxpayers and economy is to negotiate the purchase (at a fraction of face value) of the bonds from the reckless lenders that funded the banks’ foolishness.’

At the very minimum, what would this save the taxpayer? A write down between 50 and 90 percent would:

• Save between €435 million and €780 million per year on interest payments– not an insignificant sum.

• Reduce our debt/GDP ratio by between 4.3 and 7.6 percent

So, we make a real public expenditure savings and reduce our overall debt. Not a bad day’s work for a simple renegotiation.

But we can do so much more. What if we took the money saved through Jim’s Equation and reinvested it back into the economy. Spreading out the savings over five years, here is the result using the Lane-Benetrix multipliers.

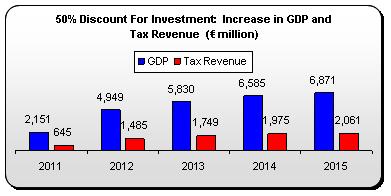

If we were to discount 50 percent of the debt and redirected it to investment spread over five years, economic growth would climb – by up to €7 billion by 2015 (an increase of nearly 3.5 percent in nominal GDP). What’s more, tax revenue would increase by nearly €8 billion over the five year period – a significant return on the initial investment.

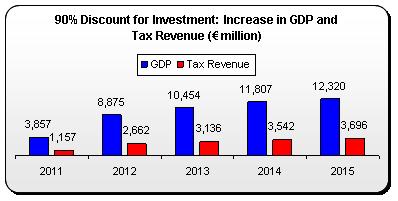

If we were to discount 90 percent of the debt and redirected it, economic growth would climb by over €12 billion by 2015 (an increase of nearly 6 percent nominally). And naturally, tax revenue would yield a greater amount over that 5 year period - €14 billion.

But the fiscal and economic benefits don’t stop there. Using the ESRI fiscal multipliers, we’d find that employment would increase:

• Under the 50 percent discount into investment, 32,000 jobs would be created, of which 20,000 would be potentially permanent.

• Under the 90 percent discount, 70,000 jobs could be created, of which 43,000 would be potentially permanent.

Then we have to count the savings from reduced unemployment costs (in 2010, the Government estimates that it pays out approximately €15,000 on average for each person in receipt of Jobseekers’ Benefit/Allowance.

And then there’s the supply side benefit – the economic benefit that persists long after the ‘building phase’ is completed. This can be measured as anything between 5 and 10 percent of the original outlay, depending on the particular project. But it can be better understood by looking at what we could have on our asset sheet:

• IBEC estimates the cost of installing Next Generation Broadband to be approximately €2.5 billion (for 90 percent business/household coverage). Imagine the productivity gains at enterprise level.

• Fine Gael has estimated the cost of fitting out a modern water, waste & sewage system to, again, be in the order of €2.5 billion. Imagine the annual savings to local authorities in reduced maintenance costs on our current Victorian-age system.

• Comhar estimates that for €4 billion, approximately 500,000 energy deficient buildings could be retrofitted. Imagine the savings on fossil-fuel consumption and the redirection of those savings into business investment and consumer spending.

And here’s the real knee-slapper: by adopting this approach, we’d bring the fiscal deficit into Maastricht compliance within a few years while substantially reducing our debt/GDP ratio. This is in contrast to the ESRI’s estimate that the current Government policy won’t be able to do that at all.

On any metric, writing down Anglo debt and redirecting into investment is win, win, won.

Of course, some will point out that we’d still have to borrow the money. But we can be comforted by the Central Bank Governor’s assurance that borrowing this money is ‘affordable and manageable’. Now, if it's ‘affordable and manageable’ to borrow money in order to burn it in Anglo’s balance sheet, then how much more ‘affordable and manageable’ would it be if we used that money for investment – with all those benefits mentioned above accruing to the economy and society.

And, yes, we’d still have to fork up billions for Anglo-Irish – there’s no escaping that. But using the ESRI’s baseline projections in its Recovery Scenario, we can measure the significant and long-lasting gains from this simple, yet far-reaching proposal in relation to Anglo-Irish debt.

We are stuck in a corner with little room for manoeuvre. The main benefit of ‘Jim’s Equation’ is that it gives us more space and more options – something we desperately need. Even if you don’t buy into all that investment lark, writing down Anglo-Irish debt will save us billions on the debt and hundreds of millions a year on interest payments at a minimum.

‘Jim’s Equation’ should be taught to every Government Minister, starting with the Minister for Finance.

Michael Taft @notesonthefront

Michael Taft is an economic analyst and trade unionist. He is author of the Notes of the Front blog and a member of the TASC Economists’ Network.

Share:

![Duggan, Vic]](/assets/img/2017/04/1491994913319631_sq.jpg)