Michael Taft: While the public sector pay agreement is presented as a platform for negotiating a reversal of the pension levy and wage cuts, the unfortunate reality is that it will likely lead to further pay cuts. Over at Notes on the Front, I investigate whether the agreement is likely to collapse under the weight of ‘unforeseen budgetary deterioration’. While this is not likely (though not impossible, things could start to get out of hand again by mid-year), such are the current trends that attempts to reverse the pay cuts under the pay review clause in 2011 will not succeed owing to budgetary slippage. In these circumstances, the pay deal will, therefore, lead to further pay cuts – potentially quite substantial ones.

Let’s assume that pay cuts are not reversed but that the agreement stays in place until 2014 – in particular, the clause:

‘There will be no further reductions in the pay rates of serving public servants for the lifetime of this Agreement.’

This clause, of course, refers to nominal pay rates – not pay rates in the real world. In the real world, what would happen to pay rates?

The Government is projecting an inflation rate of 8 percent between 2010 and 2014. Therefore, if the agreement is strictly adhered to (‘no further reductions’), public sector workers will face substantial real (i.e. after inflation) pay cuts.

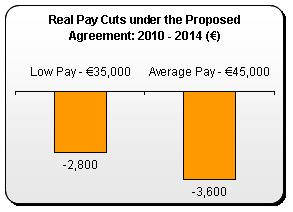

Those on low pay could face up to €2,800 in real pay cuts between 2010 and 2014 (or €700 per year) while those on average pay would experience pay cuts of €3,600 (or €900 per year).

These numbers depend on the level of inflation. The Government projects it will be approximately 2 percent per year starting in 2011. The Central Bank, however, projects inflation in 2011 at 1.1 percent. The lower the inflation rate, the smaller the real pay cut. But cuts there will be.

That only tells part of the story. Some workers will face more cuts than others. Already, workers with mortgages (in particular, younger workers, many with families) are experiencing rising interest rates with more increases on the way. This will not affect older workers as much.

Nor does any of this count any extra taxation or further spending cuts. Again, in an inflationary context, some of this could take the form of freezing tax credits and tax bands. It won’t look like a tax hike, but in real terms it will be.

If pay were to say constant in real terms – using the Government’s projections – then it would have to rise by 8 percent over the next four years. If there is to be a negotiated reversal of pay cuts, this would be additional to the 8 percent. None of this is likely.

Public sector workers are not only being asked to sign up to real pay cuts, they are being asked to lock themselves into a long-term agreement. I am open to correction, but this four-year deal is one of the longest, if not the longest, agreement negotiated since 1987. That only the Government has an opt-out clause only reinforces this lock-in.

Public sector workers will face a difficult choice when it comes to voting on this agreement. However, for there to be an informed choice, all the facts should come out. And one of them is that, on current trends, acceptance of the pay agreement could lead to substantial real pay cuts.

Michael Taft @notesonthefront

Michael Taft is an economic analyst and trade unionist. He is author of the Notes of the Front blog and a member of the TASC Economists’ Network.

Share: