An Saoi: I have had enough of all of those stockbroker economists & politicians who lecture us incessantly that exports are the key to getting us out of their economic mess. I decided to put together this note on “Irish” exports, or more correctly Ireland’s role in worldwide tax planning. You will doubtless have heard that “Irish” exports have fallen very little through this depression. This post tries to explain why.

Please make the effort to read it all; I have tried my best to keep it as simple as possible.

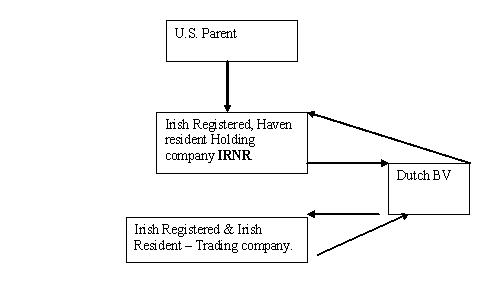

The diagrams below show a basic simple structure used by many multi-nationals to avoid paying tax. Sales are booked through an Irish trading company for perhaps the whole of Europe, and the profits are quickly hoovered into another “Irish” company, but this one is actually in a tax haven. It is sometimes referred to as a “double Irish”.

Let us say a US multi-national wants to set up an Irish trading subsidiary or as they are normally described by the IDA a “European Headquarters”. Instead of setting up one company however it sets up two, a trading sub, which will carry out the activity and a holding company, which will move its centre of management and control to a tax haven, let us say the Bahamas, directly after formation. This company is Irish Registered and Non-Resident or an IRNR.

The IRNR will own the license or intellectual property required by the trading company and issues a sub-license to a Dutch BV.

The Dutch BV passes on a sub-license to the Irish trading company. This avoids the IRNR being deemed to be resident in Ireland and thus taxable in this State. It is the reason you interpose a Dutch BV, which acts as a conduit to get the profits tax free up to the IRNR.

The Irish trading company “sells” the license, goods or whatever the company makes or does throughout Europe, paying local subsidiaries a small commission to do the marketing. It passes most of the profit upwards in the form of a royalty payment. Instead of paying a tax rate of 12.5%, it actually has a tax rate of about 3% or even less.

The US accepts that companies are resident in the country where the company is resident, but Ireland looks at its so-called “centre of management and control”. The haven company therefore is Irish as far as the Yanks are concerned, but is not consider Irish by the Revenue Commissioners.

Fig. 1

Fig. 2

Kathleen Barrington of the Sunday Business Post described here how NCR washed most of its profits through Ireland and Simon Bowers writing in the Guardian showed how Google books all its sales through Google Ireland Ltd here.

Tax avoidance is a serious issue, which as an Oxfam publication issued in March 2009 showed costs lives. Ireland is a prime player in world tax avoidance because we happily co-operate with many of the largest multi-nationals, by not just allowing these types of structures, but actually marketing the country as the place to locate.

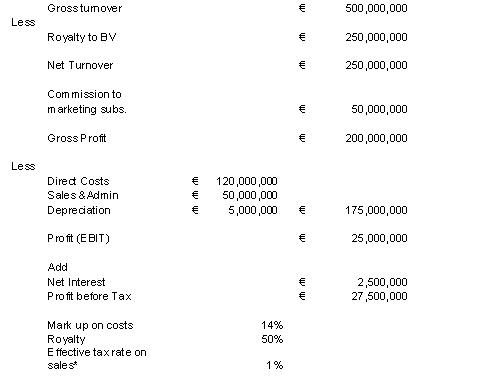

The accounts of the Irish trading entity would look something like this. This is not an extreme example, but should give a flavour of the type of “exports” we really produce.

(*I have assumed that Depreciation = Capital Allowances)

Share: